247.ai Breaks $300 Million, 10% EBITDA, Just $20m Raised

247.ai helps automate customer service interactions using artificial intelligence. The company was launched in 2000 after CEO PV Kannan visited contact centers all around the US and found himself thinking there must be a better way.

Chat was still being treated like a phone call.

By all standards the company has been a success over the past 17 years. But then a security breach happened.

I discussed it on July 25th with Kannan via a taped skype call for my podcast The Top Entrepreneurs.

247.ai Revenue Hits $300 Million

Kannan says their perfect customer is “a brand that has millions of consumers where its very challenging to handle all the inbound support across text, email, and phone.”

When these customers sign up, they start on $250k first year contracts. Across their entire customer base, the average customer pays $200k per month, or $2.4m per year.

150 Customers Pay for 247.ai Today

The company has over 150 customers and $300m in revenues. Two thirds of this revenue is pure SaaS. The other portion is service revenue.

What’s most impressive to me is how efficiently the team has used capital to scale.

You might think that with $300m they’ve raised something like $300-$500m. In reality, they’ve raised just $20m and were profitable when they did it.

A key driver of a founders ability to retain control and equity of their company comes from the ability to scale without dilution.

Kannan has been more efficient in hitting $300m in revenues than recent darling Zoom which raised $150m to hit $300m in revenues before their recent IPO.

Why raise $20m at all?

Kannan saw raising from Sequoia as a branding play. Specifically working with Mike Moritz, Kannan’s access to learnings from other Sequoia founders proved valuable and worth whatever dilution came with the $20m in capital.

That raise was back in 2003.

Since that date, it wasn’t all smooth sailing. In 2017 the company put out a press release stating they’d break $400m in 2018.

That didn’t happen.

247.ai Revenue from 2017-2018 Flat at $300m Due To Security Breach

The breach wiped out the sales pipeline and took over a year to recover from.

Today, the company is back on a growth trajectory with new ARR bookings growth in Q2 breaking 20%, the “fastest growth rate in the companies history”, says Kannan.

Have you broken 140% net revenue retention?

Currently the company churns 8-10% of its revenue annually. Expansion revenue is the same meaning net revenue retention annually is 100%.

This surprised me. Most companies at this stage are driving net revenue retention into the 130%+ range.

For example, Xactly is at 130% net revenue retention and PingIdentity is at 128% net revenue retention with $280m and $180m in annual revenues respectively.

Part of the reason for this is that the customer success hasn’t been a priority. This function is usually the one that drives usage and expansion growth on annual contracts.

Today, the team is about 800 people. The service side of the business includes about 1000 agents which are used to teach the technology AI engine.

How much does 247.ai pay for a new customer (CAC)?

Customers fall into 3 categories according to Kannan.

Ones that can spend more than $10m, ones that spend $1m or less, and ones that spend less than $500k.

In each cohort they are at a 12 month payback period and are happy optimizing to stay at that payback period timeframe.

Why Haven’t You Sold To Private Equity for $6B?

“The team would prefer to IPO”, says Kannan. The company is built for the long run and profitable he continued.

Most PE folks Kannan has spoken with are very interested. Most of the problem solving has been done. When evaluating PE offers, Kannan asks how much value they can extract on their own, without private equity versus with private equity.

He feels they can get more value being standalone.

Would you ever do $1B secondary?

“We’d do it for a good reason like if we can to acquire someone in the space for $400 million”, says Kannan.

Even then, the company is currently taking 10% to the bottom line each year, or about $30m leaving plenty of dry powder for acquisitions.

The company is on track to increase profitability profile to 20% EBITDA margins by mid 2020.

Data breach behind them, look for Kannan and team to scale to $400m over next 3-6 quarters and toy with an IPO if the market stays favorable.

Tags

Recent Articles

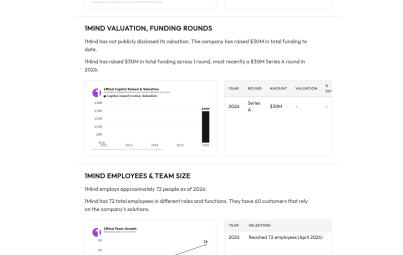

How 1Mind Achieved Rapid Revenue Growth with AI-Powered Sales Solutions

In the ever-evolving world of technology, few companies have managed to disrupt traditional sales and marketing processes as effectively as…

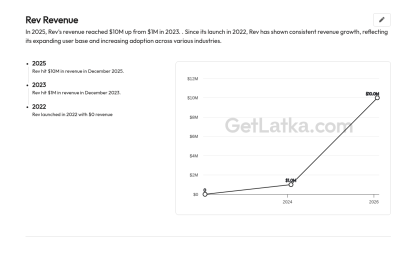

How Rev's CEO Adi Bathla Drove Revenue to $10M by Revolutionizing Auto Shop Workflows

Building a company from scratch and driving it to hit significant revenue milestones is no small feat. Adi Bathla, the…

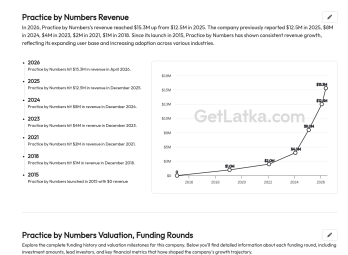

How Practice by Numbers Achieved $16.5M Revenue in 2026 with Innovative SaaS Solutions

2015: Launched Practice by Numbers to Fill a Market Gap Practice by Numbers (PBN), co-founded by Rohit Garg and Dr.…