Divvy Founder Alex Bean Interview 1 Day Before Exiting for $2.4 Billion to Bill.com

Divvy is a B2B SaaS fintech that provides everything from expense management to virtual cards and AP automation. The company was founded in 2016 and is based in Lehi, Utah.

Nathan Latka sat down with Alex Bean, CEO of Divvy, to discuss his rockstar growth.

- $100mm run rate in 2022

- More than 10,000 customers

- Processes more than $1b in transactions

Nathan Latka (00:00):

Hi everyone. My guest today is Alex Bean. He’s sitting on a rocket ship with Divvy, but 10, 11 years ago he’s selling scooter parts. What happened? We’re going to dive in today. Divvy modernizes finance for businesses by combining expense management software and smart corporate cards into a single platform. Finance leaders can now get real time visibility into their company spend and flexible control that prevent teams from ever going over budget. You can check it out at getdivvy.com. Alex, you ready to take us to the top?

Divvy CEO Alex Bean (00:23):

Yeah.

Nathan Latka (00:24):

Just say scooter business-

Divvy CEO Alex Bean (00:26):

I wasn’t ready for the scooter business reference, but we can dig into it.

Nathan Latka (00:29):

Well, it’s crazy. I mean, my research team, they’re going, “Wait. This guy went from basically being a GM at a scooter place to running one of the fastest-growing FinTech businesses today. How the hell does this happen?”

Divvy CEO Alex Bean (00:39):

Yeah, so real quick on the scooter business. I mean, I actually feel like those are some of my most formative years. I was in my mid-twenties. Knew the owner of the business, he got sick and he said, “Hey, I’m sick. Can you come in and run it? Can you come in and build this thing?” And at the time we thought we were going to take over the X-Games and take over skateboarding, so you kind of thought big. But we did some fun stuff, learned a lot about manufacturing and branding. And he got healthy, so that’s when I gave it back to him and got into tech. So learned a lot, a lot of fun, but definitely different than FinTech, for sure.

Nathan Latka (01:16):

So if you had Divvy when you were running that business, what sort of credit lines would you been pulling? What sort of expense management would you have been doing? Explain the current product as how you would’ve used it back then.

Divvy CEO Alex Bean (01:27):

Yeah, but it’s funny because you might say like, “Well, how’d you go from selling scooter parts to doing Divvy?” And, to me actually, it’s super natural. Because when I’m running Lucky, which was the scooter company, we had 10 riders all over the world, traveling for various tournaments, building content, we would do trade shows. And so I would send seven guys to Vegas on a trade show conference. And we’re a small company, we didn’t have a ton of cash, so spending the budget of $15,000 for the conference was imperative. You can’t go over. But everyone was using their own card, we were getting expense reports a month and a half late. So we were going over without knowing we were going over and Divvy would’ve solved that entirely. We could have said, “Hey, here’s your budget, had cash, check, credit, everything inside of that, expense reports from all the riders and all the employees would’ve come directly.”

Divvy CEO Alex Bean (02:18):

So, honestly, when we started Divvy, my partner Blake and I, it was just like, “Well, we’ve ran multiple businesses and we understand the needs.” And so we built it not as tech engineers, but as business owners and saying we’re building something that we would’ve wanted to use in our prior companies.

Nathan Latka (02:35):

And who’s the customer target today? Is it the Luckys of the world? SMBs?

Divvy CEO Alex Bean (02:39):

Yep. Luckys of the world, just SMBs. We kind of have two audiences, I’d say. One to 50, and 50 to 500, slightly different use cases for the most part. But SMBs in general, that’s who we’re going after. The mom and pops of America, Main Street America, not just the VC-backed companies.

Nathan Latka (02:55):

Yeah. And talk to me about that segment. So if an SMB is listening right now and they’re going, “Man, I’m currently using six tools to do all these things Alex is talking about,” and they want to start with you. What’s the average price point an SMBs going to pay you guys?

Divvy CEO Alex Bean (03:08):

Nothing. It’s free.

Nathan Latka (03:09):

Okay. So how do you make money?

Divvy CEO Alex Bean (03:11):

Yeah. So we basically take Amex. You’re not paying for your Chase card, or your Wells Fargo card, or whatever. We take your credit card, that’s how we make money. So we make money just like the banks would and then we give you the software that Expensify and others are giving you. So we really combine it into one platform. And what we’ve found is by combining it’s not only just that it’s free, the source of information is so much quicker and so much better so the things we can do are much different. But yeah, it’s free. And that’s why we’re super excited to offer it to the mom and pops of the world. Because we can tell them, “Stop paying for those three softwares and come just use Divvy.” And it’s a win-win for both.

Nathan Latka (03:52):

Yeah. I mean you have four sort of buckets on your website, business credit, spend management, expense management, and AP management. There are multi-billion dollar companies competing in just one of those verticals. Just to be clear, I want to make sure I’m getting this right, you’re giving away spend management, expense management, AP management free. You’re making money on the credit card stuff and the credit fund?

Divvy CEO Alex Bean (04:09):

Yep, exactly right. Yep.

Nathan Latka (04:10):

Wow. Okay. Interesting. So I guess the question I would have for you is this is not easy software to build. How did you fund it in the early days so that you could give it away for free?

Divvy CEO Alex Bean (04:18):

So that’s actually a really good question. I’ve had that conversation with a lot of people. A few things. One, we raised money early because we knew that we were taking a big swing. I don’t think that’s for everyone. So I’m not out there recommending to all entrepreneurs, go raise VC funds, go raise as much as you can. But for us, as you just said, we’re taking on trillion dollar markets in all four of those buckets. So we’re like, “All right. We’ve got to bring money to the table and go build the team.”

Divvy CEO Alex Bean (04:47):

So, for us, that’s what we did. And at the beginning, nowadays in the FinTech space, if that’s where you’re at, there’s so many more tools that enable FinTechs to go build companies that didn’t exist five years ago. Which that sounds nuts, but I can get into the nuances, a lot of things that the banks couldn’t offer us five years ago that now they’re fully built to offer to these Fintechs. So I think you’re going to see a wave of innovation because of that.

Nathan Latka (05:12):

So year one, it sounds like was, what, like 2016, 2017. Is that right?

Divvy CEO Alex Bean (05:15):

Yeah.

Nathan Latka (05:16):

And I want to touch on founding story real quick because founder equity is obvious a hot topic with anyone watching a company. Do you guys just say you know what, we’re equal partners 50/50? Or was there some nuance there?

Divvy CEO Alex Bean (05:25):

A nuance. Yeah. And so every partnership’s different. So anything I give here is not going to be definitive for all. So Blake, my friend and partner, came to me with the concept of Divvy. And we formulated it together, but his original idea was his, and the name Divvy came from him. And, frankly, he had the money to help kickstart some of this.

Nathan Latka (05:53):

How much did he kickstart it with?

Divvy CEO Alex Bean (05:57):

I think that’s private. Sorry. I don’t know if we’ve disclosed that. But it was a decent amount of his own money to say, hey, we’re going to go design, and engineer, and do some stuff before we went and raised formally. So he has more than me, clearly. He had it. And the advice I would give a non-CEO co-founder is you have to understand where you sit. For me, I always knew Blake was the quarterback and I was the running back, to use a football reference. Meaning we were partners and I don’t think he could have done it without me, but I know I couldn’t have done it without him. And you can still be partners and not be 50-50. I think I’ve seen a lot of partnerships where you go in and they are equal partners. One might be the CEO, but the other one, they had the idea together and that’s 50-50. Great. That would be awesome. But for us, it was not 50-50, but that doesn’t take away from the partnership. So nuanced there-

Nathan Latka (06:50):

First formal round was when and how much?

Divvy CEO Alex Bean (06:53):

$10 million from Paleon Partners here in Utah, and I think that was in, was it 2018?

Nathan Latka (07:04):

And you just raised more this year, I think. What was that?

Divvy CEO Alex Bean (07:07):

Yep. Brought on Hanaco, Whale Rock, Crew. So some great investors. It was their series D.

Nathan Latka (07:14):

And how much did you guys raise there?

Divvy CEO Alex Bean (07:15):

$165,000, I think.

Nathan Latka (07:17):

And do you remember the valuation?

Divvy CEO Alex Bean (07:19):

1.6.

Nathan Latka (07:21):

1.6. So full story there, don’t want to bury the…

Divvy CEO Alex Bean (07:24):

Just as an entrepreneur, you’re like, “Do you remember the valuation?” I’m like, “Well, let me see here. Yeah. I remember the valuation. Yeah.”

Nathan Latka (07:29):

Maybe I strategically ask it that way to make sure more people answer. If you phrase it that way, you definitely get a higher response rate. But I wanted to put that out there because, again, what you’re doing here is very interesting. We’ve had David on from the expense side, we’ve had Brex on, we’ve had Ramp on the show, and they’re basically building massive business on something that you’re doing for free. So I want to dive more into the credit card business. I mean, how much money can you make on the credit card business? There’s only what 200, 300 BPS of spread there?

Divvy CEO Alex Bean (07:53):

Yep. That’s correct. But there’s a few different ways. You see Brex is starting to launch paid software. We have paid software. You make money on the credit side, fees and things of that nature. I mean, it’s just like a bank. It’s basically asking the question, “Well, how is Amex making money?” And it’s like, “Well, I mean, I think they’re making a fair amount of money.” So even 200 or 300 BPS, you start to do the math and you’re doing billions of dollars in spend and the revenue starts to add up.

Nathan Latka (08:25):

What will GM be this year through the platform?

Divvy CEO Alex Bean (08:29):

I don’t think that’s disclosed, but we did… Oh man, I don’t think that’s disclosed so I’m going to keep that private.

Nathan Latka (08:37):

Can you do a range, Alex?

Divvy CEO Alex Bean (08:39):

Billions of dollars in spend.

Nathan Latka (08:40):

Okay. Got it. So more than $1 billion, less than $100 billion. Is that a big enough range?

Divvy CEO Alex Bean (08:43):

Sure. Yeah, that’ll work. Yeah.

Nathan Latka (08:46):

That’s a damn big range. But more than $1 billion, less than $10 billion. And then, I guess, can maybe just so I can quickly understand this. So last 12 months, if you guys look at your total revenue, just give me percentages, what percent would you say is credit card versus paid software versus your credit fund returns?

Divvy CEO Alex Bean (08:59):

I would say majority of that is on interchange.

Nathan Latka (09:04):

Oh wow. So really it’s mostly credit card. Interesting. I was thinking you might have said that there’s actually a massive balance sheet business here because you have a unique insight to data. You can underwrite better than anybody else.

Divvy CEO Alex Bean (09:14):

Yeah. There’s definitely an element to that. But even if you talk to Brex and Ramp, you’re not making most of your money on that. Because, again, underwriting just minimizes your losses. If you’re really good at underwriting, it doesn’t add revenue, it minimizes your loss rate.

Nathan Latka (09:30):

So look, I mean, there are Kabbages of the world that play in this space. It’s a purely balance sheet business, you drive your cost of capital up plus one or two, you have underwriting, you do deals, SMBs at a 35% effective APR, you make a big spread.

Divvy CEO Alex Bean (09:43):

Yeah. So the difference on that, I think you’d see the same with Brex and Ramp too. Right now when we’re underwriting, we’re not doing a lot of loans. We will be adding to that, we kind of have that in beta. It’s more underwriting your credit card, like an Amex. So if you don’t pay then there are fees. And obviously there is revenue that comes from like, “Hey, if you don’t pay your credit card bill or you pay it late it’s carried interest, etc.” But Kabbage is doing loans. They’re just straight out saying, “Hey, we’re going to give you a $100,000 loan at this return. So.”

Nathan Latka (10:12):

Got it. So just to be clear, you’re just doing the credit card. So you guys haven’t went out and raised $1 billion dollars as a balance sheet credit fund to do small business loans into your partners?

Divvy CEO Alex Bean (10:21):

Well, while we do have that set up, we are not fully launched on it simply from a product standpoint. We actually launched it pre-COVID. We pulled it obviously with COVID and now we’re going to start launching it again. So it’s definitely in our wheelhouse, it’s the same conversation Amex and all these guys have. So maybe in the way we do it we feel like we’ll have some innovation on it, but the concept of those loans is not innovative.

Nathan Latka (10:45):

Talk to me about how many of these customers you’re serving now today. What’s the number?

Divvy CEO Alex Bean (10:48):

Over 10,000 and adding quite a few every month. So we’re super excited about our growth rate and it just means that… I mean, our motto is spend smarter, so for us it’s about having more and more SMBs, mom and pops, build Lucky Scooter- size companies. Spend smarter, stay in budget, hit payroll, save money. I mean, that’s kind of what we’re all about. So for us seeing that number rise is exciting.

Nathan Latka (11:13):

Your press release says 2019, 1,000 customers. 2020, 4,500, so you’ve more than doubled in year-over-year, now breaking 10,000. What do you think you’ll finish this year at? How many adding new per month?

Divvy CEO Alex Bean (11:23):

Yeah, I mean, I think we’ll easily top 20,000 and even with some growth on that. So, we’ll see. But we’re growing over 100%. So we expect that to continue.

Nathan Latka (11:34):

And are you also growing revenues 100% year-over-year?

Divvy CEO Alex Bean (11:37):

Yeah.

Nathan Latka (11:37):

How long can you keep doing that? I mean, it’s hard to do that at big numbers.

Divvy CEO Alex Bean (11:40):

Not forever.

Nathan Latka (11:41):

Yeah. That’s a good answer. Can you give us a sense of revenue today?

Divvy CEO Alex Bean (11:48):

No. Again, sorry, I don’t want to be coy. I just think that right now it’s private so I’m going to hold onto that. But no, I mean, we’re super excited about it. We hit some big milestones recently. You can look at our valuation and probably drive some element of what it is. So, no, but…

Nathan Latka (12:06):

I haven’t done a series D round recently. Help us understand. Don’t talk about your own deal but in most series D rounds, how much of a company is a SaaS founder going to be selling?

Divvy CEO Alex Bean (12:19):

Actually I’ll give you this. So if you’re going to go public. Now, SPACs do make it a little bit different, but I think you see a lot of companies that go public and we would look at it and say, “Hey, you got to be doing $200 million in revenue, $300 million in revenue to be go public.” That’s when you start to be a known name and really have traction. So, for us, in between that $100 to $300 range, that’s where we look at that and say, “Okay, what are your growth rates? When do you hit what milestone? What do we need to do to accelerate out of this?”

Divvy CEO Alex Bean (12:52):

And look at Qualtrics. They just went public here in Utah. They’re friends of ours. And it’s like they hit the $200 million, then they hit the $300 million, then they hit the $600 million, and now they’re even approaching the billion. And it’s like, you just have to keep that trajectory of growth. So I’m not going to announce our forecast of two years from now on this podcast, but it’s keeping a really healthy growth rate. It might not double forever clearly, because at some point that will stop.

Nathan Latka (13:20):

But do you guys feel good about your plan to break $100 million run rate in the next two years?

Divvy CEO Alex Bean (13:26):

Yes. I feel very good about that. I’m very confident-

Nathan Latka (13:33):

That helps me. Yeah, go ahead. Make the statement.

Divvy CEO Alex Bean (13:35):

No, I’m very confident that we will achieve that. Yeah.

Nathan Latka (13:38):

There you go. That helps me with a bunch of things. So it tells me you’re not at $100 million yet but the growth plan obviously clearly takes you over that mark. So, that’s great. Is there anything you talk about in terms of product? It sounds like you have a credit fund maybe in the works. You’ll be more aggressive there. Any other of the products you plan to give away free?

Divvy CEO Alex Bean (13:55):

Yeah. So I mean AP management, you see that as one of the four buckets. The reason we view that as so powerful is we want it to be one place that you’re making all your spending, and you’re reconciling, and you’re thinking through what’s going out of the company. So we’ve launched that, but it’s not where we want it to be in terms of full scope and capability and the innovation we can bring to that side of the fence. So that, to me, is what we’re probably most excited about coming around the corner.

Nathan Latka (14:29):

Got it. That makes good sense. And then talk to me a little bit about churn in this space. How do you even define churn? Because if you’re not a traditional SaaS company where there’s a start and end date, do you define churn as they have a credit card and they stop using the credit card?

Divvy CEO Alex Bean (14:39):

Yeah, basically. So churn for us is very strong. We have launched budget-

Nathan Latka (14:47):

Strong or…? So what are you churning annually right now?

Divvy CEO Alex Bean (14:51):

We are not churning very much. We’re in a very good position when it comes to churn, and the reason is because-

Nathan Latka (14:58):

By the way, I consider a very good position under 5% annually. Is that fair to say?

Divvy CEO Alex Bean (15:01):

Yeah, it’s very fair. So which is crazy on a free product that people can walk away. You would assume a lot of people just sign up for free and they walk away-

Nathan Latka (15:12):

Well and SMB, I mean that’s crazy low for SMB.

Divvy CEO Alex Bean (15:13):

Yep. Yep. But we’re why we’re in a really good position is budgets. So if someone gets into

Divvy and they set up virtual cards, and they set up budgets, and they set up this new process, to go back to another way of doing it or an old way of doing it they’ve got to go get their Amex card again. They then have to set up Expensify. Then they have to bring everything together. And with Divvy, once you have budgets and you’re operating out of a budget mindset, which can be a little hard upfront, but on the back end they’re not leaving because it just has changed the way that they’re running their finances. And no one else is doing that yet. I know people are going to copy us. I won’t name one competitor, but we tend to see a lot of copy from someone out there. But I know-

Nathan Latka (15:58):

Who’s the competitor?

Divvy CEO Alex Bean (15:59):

No. I’m not going to do it.

Nathan Latka (16:01):

What’s the first letter? What’s it rhyme with?

Divvy CEO Alex Bean (16:05):

Let me put it this way. This is my honest opinion. People will probably kill me on it. I don’t know how many people are even listening to this. I have a lot of respect for what I see Brex do in the market. They bring a lot of their own innovation to the market and it’s super, super impressive. And so they challenge us, and we challenge them, and whatnot.

Nathan Latka (16:24):

Who’s bigger?

Divvy CEO Alex Bean (16:27):

Well, they just announced a large evaluation so it’s fair to say that they are.

Nathan Latka (16:32):

Do you think they’re doing more revenue than you, or they’re just good at driving evaluation?

Divvy CEO Alex Bean (16:37):

I don’t know their revenue for sure, but I’m fairly confident. I think the gaps are smaller than people think. I think they are very good at driving evaluation, but they’re bigger. I think that it is very fair to say. I can’t speak to their numbers and stuff, but… My thing is Brex drove innovation on the credit side and they deserve a lot of credit for it. We drove innovation on the software side and we deserve a lot of credit for it. And what my point is, you’re going to see the market, whether it’s the big companies like Chase, Wells Fargo, Amex, etc. or other startups copying suit. Budgets is one of those things that we’ve held to and we’re super proud of, and it’s super powerful for our customers. And I think you will see that be emulated in some form over the next couple years.

Nathan Latka (17:27):

Yep. Your forensic Qualtrics had this, and the public markets in the SaaS world, anything above 130%-140% net dollar retention is world class. It’s hard to drive expansion revenue in the SMB cohort. What does your expansion look like over the last 12 months on the historical cohort?

Divvy CEO Alex Bean (17:42):

So, again, not going to disclose specific numbers. Here’s the thing though. With Divvy, someone will get in and they’ll start using us for the card software. But then they start using us for the AP management, or at some point they’re going to start using us for the loan management. So we actually feel like there’s another five things we can add in that stack. And five, just being a kind of a figurative number.

Nathan Latka (18:03):

That’s all mainly free though, right?

Divvy CEO Alex Bean (18:06):

Yeah. But everything we launch has something that adds to the wheel, whether it’s direct revenue, whether it’s future software revenue, whether… And let me give you an example, and I’m not going to give you a price point, but AP management. So let’s say it takes five days for your ACH check to get into your vendor’s hands. Well, hey, for a premium fee, we can get it to them in two days. Okay, cool. And every single thing that we do has a flywheel effect. You want to suck in your invoices into the system? Well, every invoice is a new vendor that we can talk to and say, do you want to accept a virtual card or do you still want to accept the ACH?

Divvy CEO Alex Bean (18:44):

And there are ways for us to make money in that flywheel and get new customers. So even though something’s free, I mean the obvious one is, look at Facebook. It’s free, but clearly there’s flywheels that are making a ton of money. And we have a very similar one just on the business side.

Nathan Latka (18:58):

Fair. Can we say your net revenue retention is above 120% or 110%?

Divvy CEO Alex Bean (19:05):

To be perfectly honest, I can’t actually recall the number off the top of my head. I’d have to go check.

Nathan Latka (19:10):

No problem. Last question that I want to dive into. So you’re giving the software way free, but you find unique sort of almost like utility based ways to pull some margin out. You just gave a good example on the AP management side of things. I mean, how much right now can you guys make on average per SMB using the platform? Is it like $10,000 in a year, or $1,000 a year or what?

Divvy CEO Alex Bean (19:29):

Yeah. And again, I’d have to look at the number. It’s thousands. It’s really healthy, meaning we feel really, really good. The averages can change depending on, is it the 1 to 50, 50 to 500? Clearly if someone’s a 100% company spending $100,000, you know there’s 200 to 300 BPS. So you can do the math. Now, there’s a lot that we have to account for, though. What people don’t forget is we are giving rewards back to our customers.

Nathan Latka (19:53):

You don’t make the full 300 BPS, do you? I mean, I imagine you’re probably making like 70 BPS, or 100 BPS, max.

Divvy CEO Alex Bean (19:57):

Yeah. I mean, it comes to us, but there’s costs. There’s risk, you have to put money away for risk, you have to put money away for cog, you have to put money away for paying it back to the customer in rebate. And so there’s a lot of factors in there, but yes, there’s still a very healthy business and what you can make a fair amount of money on a free product to an SMB. Yeah, super attractive.

Nathan Latka (20:16):

Alex, the last thing I want to touch on before we wrap up. A lot of founders, they don’t understand the concept of secondaries. But I like it, IT removes risk from the business. It allows you to double down and go for a $10 billion sort of thing and build something bigger. How have you and your Blake thought about secondaries? And even for your early employees, was there any of the $165 million recent raised as secondary?

Divvy CEO Alex Bean (20:36):

Yeah. And again, I don’t want to speak to specifics because there’s always a lot of people involved and whatnot, but I will say as a whole, I agree with you. Secondaries, done right, can give motivation which allows early founders and early employees to keep going as opposed to stop. Because it’s easy to say, “Oh, I’ve been grinding away for however many years and I just need something out of it.” Fine, press the button. But secondaries, I think, are really, really healthy if done correctly. Which is, by the way, I don’t know if everyone would agree with that statement in Silicon Valley. So I’d love to hear other people’s opinions, but I do think it’s healthy.

Nathan Latka (21:19):

All right. Let’s wrap up here with the famous five rapid fire. Number one, favorite business book?

Divvy CEO Alex Bean (21:24):

Actually, you know what? It’s not my favorite of all time, but the John Iger book, I found at least very entertaining. The one he wrote last year.

Nathan Latka (21:32):

Number two, is there a CEO you’re following or studying?

Divvy CEO Alex Bean (21:38):

I’m late to the party because I’m not on Twitter, but I’ve been following Naval more. And I found a lot of what he says to be pretty interesting, so sure, we’ll go with him.

Nathan Latka (21:49):

Number three, besides your own, what’s your favorite online tool for building Divvy?

Divvy CEO Alex Bean (21:52):

Sorry, say that again.

Nathan Latka (21:54):

Favorite online tool that you used to build the company.

Divvy CEO Alex Bean (21:58):

So my favorite tool that we’re using internally?

Nathan Latka (22:01):

Or personally, yeah.

Divvy CEO Alex Bean (22:03):

Okay. I’m going to give both. So I don’t know how I would live without Slack. So Slack is clearly up there. Everyone’s heard of it, but you know what I got to give a shout out to is OneNote.

Nathan Latka (22:15):

Evernote’s super sexy. It’s the Silicon valley. But, look, One Note is a vastly superior product to Evernote and what you can do with it. So I’ll go with One Note.

Nathan Latka (22:25):

Number four, Alex, I think you said you have a three month or a three year old. How many hours of sleep you getting these days?

Divvy CEO Alex Bean (22:29):

I have four kids under the age of 10. So if it was just one three year old, I wouldn’t be stressed. That would be quite easy, actually. But I have two girls and two boys, but I also have an amazing wife who helps to obviously do a ton. So I’m getting adequate sleep. But, yes, my 10 year old was up till midnight last night and I’m having to lie in bed with her and talk her through the whole thing. So there are some nights where it’s longer than others.

Nathan Latka (22:56):

And, Alex, how old are you?

Divvy CEO Alex Bean (22:58):

36.

Nathan Latka (22:58):

Last question. Take us back 16 years. What do you wish you knew when you were 20?

Divvy CEO Alex Bean (23:06):

You’ve heard it but I believe so strongly your 20s are meant to learn. Don’t focus on the salary. Obviously salary’s a matter of respect. Salary is what you’re valued at. I totally get that, but don’t take jobs for the salary. Take jobs that you’re going to learn, what you need to learn to take the leaps and jumps that you want to ultimately do and make your money. And that might happen in your late 20s or in your 30s or 40s. But, please, when you’re 20 find the right people in the right companies, work with them, and you will learn so much that the rest will be taken care of. Money will come.

Nathan Latka (23:43):

Guys we’re having Alex from Divvy. They launched back in 2017, financed with their own personal capital, did a first formal round of about $10 million, crossed 1,000 customers, SMBs mainly, in 2019. Now over 10,000 customers with a clear path to break $100 million bucks in AR over the next two years. Most of their business it’s giveaway free software where they have multi-billion dollar competitors in the AP management space, expense space, ready to make all their money on those 300 BPS on the credit they provide. They process currently between $1 billion and $100 billion, nice big range there. Alex, thanks for taking us to the top.

Divvy CEO Alex Bean (24:11):

Any time. Thank you.

Tags

Recent Articles

How 1Mind Achieved Rapid Revenue Growth with AI-Powered Sales Solutions

In the ever-evolving world of technology, few companies have managed to disrupt traditional sales and marketing processes as effectively as…

How Rev's CEO Adi Bathla Drove Revenue to $10M by Revolutionizing Auto Shop Workflows

Building a company from scratch and driving it to hit significant revenue milestones is no small feat. Adi Bathla, the…

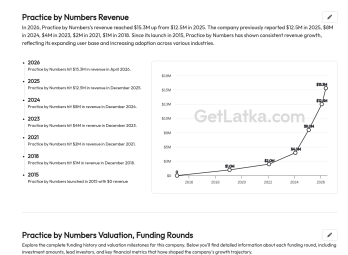

How Practice by Numbers Achieved $16.5M Revenue in 2026 with Innovative SaaS Solutions

2015: Launched Practice by Numbers to Fill a Market Gap Practice by Numbers (PBN), co-founded by Rohit Garg and Dr.…