Venture Debt | What It Is & How It Works [2022 Guide]

Let’s be honest – most startup founders don’t have never-ending cash in their pockets to fund their startups.

So, whether you’re just starting out or looking to boost your business’ growth, you’re probably looking for different financing options.

Chances are, you’ve tried applying for a traditional bank loan and got turned down. After all, most banks don’t easily give out loans to new, high-risk businesses.

And, if your startup isn’t generating revenue just yet, securing funding can seem like an impossible task.

If all this sounds familiar, you might want to look into venture debt financing – and you’re just at the right place.

In this article, we will cover:

- What is Venture Debt?

- Venture Debt & Other Types of Credit – What’s the Difference?

- How Does Venture Debt Financing Work?

- When Does Venture Debt Make Sense for a Startup?

- Who Offers Venture Debt?

- How to Pick a Venture Debt Lender – 5 Things to Keep In Mind

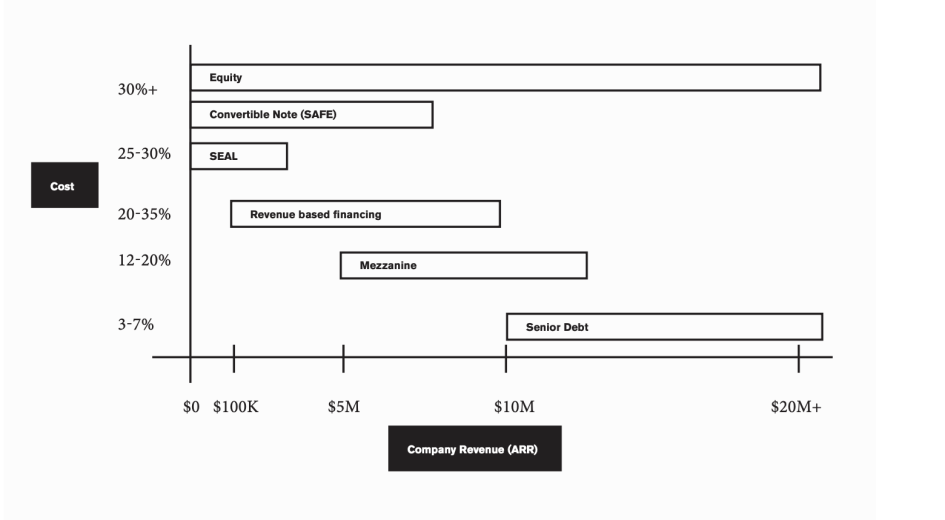

What is Venture Debt?

Venture debt, also called venture lending, is a type of debt-based financing that’s available primarily to venture-backed companies.

In particular, venture debt is popular among startups and growth-stage companies— especially those without assets or a positive cash flow.

In most cases, venture debt lenders provide venture debts as term loans that last for up to 3 years with interest payments and warrants.

Although companies can use venture debt instead of equity financing, it’s most effective when used alongside other types of financing (e.g. between equity rounds).

Venture Debt & Other Types of Credit – What’s the Difference?

Venture debt has significant advantages compared to other types of credit, including:

- Less expensive than raising equity.

- More flexible clauses than with other types of funding in terms of debt amount, amortization, personal guarantees, and such.

- Less prone to share dilution than equity funding.

- Quicker to secure (e.g. it can take up to 1 year to secure equity financing, whereas you can secure venture debt financing in just 3 months).

That said, the most prominent difference between venture debt financing and other types of financing is accessibility and warrants.

Here’s what each is about:

Accessibility

Unlike most other types of credit, venture debt financing is accessible to startups.

With other types of credit, such as traditional bank loans, companies have to prove they’re able to pay off the loan by providing information on their revenue, cash flow, debt service coverage ratio, and such.

For this reason, most startups get rejected for a loan – after all, it takes 3 to 4 years on average for a company to start generating profit.

If you’re applying for venture debt, however, you don’t have to provide these SaaS financial metrics, which is a huge advantage for many startups and growth-stage companies.

Instead, venture debt lenders use different information to determine whether a company qualifies for venture debt. This can include the total amount of financing the company has raised in previous financing rounds, investors’ track records, the company’s business plan, and the like.

Since venture debt lenders don’t consider a company’s cash flow when determining its eligibility for venture debt, companies without a positive cash flow can also obtain a venture debt.

As such, venture debt is a great financing source for venture-backed startups and growth companies that can’t qualify for other types of credit.

Warrants

Essentially, venture debts are high-risk since they’re given to new, often unprofitable businesses. As such, venture debts offer a financial incentive for venture debt lenders in the form of warrants.

Simply put, venture debt warrants allow the warrant holder to buy stocks at a fixed price indicated on the warrant. It’s also important to note that warrants last significantly longer than stock options.

Venture debt lenders can use these warrants to buy company stocks in case of liquidity (for example, if you sell your business).

Without warrants, venture debts would come with an extremely high-interest rate, which would consume a large portion of a company’s cash flow.

As such, warrants are an exclusive feature of venture debt that allows companies to minimize the cost of debt and, at the same time, provide venture lenders with more security.

How Does Venture Debt Financing Work?

If you’re looking to raise venture debt, you first need to find a venture debt lender.

The criteria that determine whether you’re eligible for a venture loan can vary depending on the venture debt lender and the loan itself.

Nonetheless, most venture debt lenders evaluate the following to determine your eligibility:

- Product-market fit

- Quality of your management team

- Earnings before interest, taxes, depreciation, and amortization (EBITDA)

- Repeatable sales process

- Annual revenue

- Existing or projected business growth

- Ownership (venture-backed, sponsored by a private equity company, etc.)

- Business plan

Now, whether your startup meets the criteria is for the venture debt lender to decide.

For example, while most venture debt lenders require a startup to generate at least $200,000 in annual recurring revenue, some venture debt lenders allow pre-revenue startups to borrow.

Next, all venture debt terms and conditions will be outlined in the venture debt term sheet, which is a non-binding outline of the venture debt prepared before the final venture debt contract.

Typically, the sheet includes:

- General information, such as the company and venture debt lender’s name, date, and debt currency.

- Debt amount, which can be set as a fixed amount or a range (e.g. $2 million or $2-3 million).

- Interest rate and payment schedule, such as monthly interest payments.

- Warrants allow the venture debt lender to buy equity at a fixed price (e.g. if you sell your company).

- Maturity date, which determines when you should make the last payment.

- Fees, including prepayment, back-end, and other fees.

- Conditions precedent refers to the actions your company must take before closing the agreement (e.g. terminate another contract).

Not to mention, the venture debt term sheet helps you compare different lenders and their conditions. Once you select a lender, you’re ready to sign the final venture debt contract and obtain the debt.

When Does Venture Debt Make Sense for a Startup?

There are two main financing options for startups to accelerate business growth:

- Raising equity

- Raising debt

Alternatively, you can also use a mixture of the two options.

Now, one thing you should keep in mind is that obtaining venture debt is significantly cheaper than raising equity. For this reason, venture debt is a great option for startups with a higher burn rate.

In particular, startups can use venture debt to:

- Fund working capital

- Finance capital investments and business acquisitions

- Extend cash runway between equity rounds

- Extend cash runway to positive cash flow

- Build a steady credit track record

- Finance equipment purchases

- Finance specific business projects, such as marketing campaigns

- Finance other investments to speed up business growth

- Prevent equity dilution, especially if you’ve already lost equity in the previous funding rounds

That said, venture debt might not always be the best option for your startup.

Specifically, you should not raise venture debt if:

- You can’t repay the debt. Although venture debt financing often offers favorable terms to startups, a debt is still a debt – and you need to repay it. So, if your startup is performing very poorly and has a very high burn rate (e.g. your cash runway is less than 6 months), you may want to reconsider raising venture debt.

- Venture debt terms are too expensive or restrictive. Before coming to an agreement, you should carefully consider whether venture debt will be burdensome to your startup. As such, you should model the total cost of the venture debt and see how it would impact your startup if you were to raise it.

- Your investors are against it. If you’re like most startups, you’re raising venture debt alongside equity. In this case, you should take your investors’ opinion into consideration. If they don’t approve of your decision to raise venture debt, it’s best to steer away from it.

Who Offers Venture Debt?

You can obtain venture debt from banks or non-bank venture debt lenders, such as venture debt firms.

Typically, venture debt costs are cheaper if you’re raising debt from banks.

However, you should keep in mind that banks have limited venture debt sizes due to regulations. For this reason, you might want to opt for a non-bank venture debt lender.

TLDR: If you don’t want to go down the traditional VC path and sell equity in your SaaS company, here’s a spreadsheet of 50 lenders who’ll give you money.

How to Pick a Venture Debt Lender – 5 Things to Keep In Mind

When it comes to picking a venture debt lender, one thing is for certain – you have to do it carefully. That’s because an inexperienced debt lender can burden your company with less-than-optimal repayment, which can lead even the most promising businesses to fail.

So, here are 5 things you should keep in mind to select the right venture debt lender for your business:

- Explore your options. Instead of picking the first venture-debt lender who’s open to financing your business, reach out to different venture debt lenders. Comparing their pricing, repayment terms, experience, and reputation allows you to make an informed decision and pick the best venture debt lender for your business.

- Look for timely funding. Make sure to select a venture debt lender that is well-established and known for dependable funding to accelerate your business’ growth. An irresponsible venture debt lender that fails to fund your company on time may cause you unnecessary stress, disturb your plans, and delay business growth.

- Consider the loan size the lender offers. In most cases, you want the loan sum to extend your business’ runway by at least 6 months. This allows you to fund day-to-day operations and boost your business’ growth so that later you can obtain more financing if needed.

- Choose an initiative venture debt lender. Compared to venture capitalists, venture debt lenders are typically less involved with your business. Nonetheless, a great venture debt lender will be an excellent financial partner, open to giving you business advice and working closely with you in case your company needs debt restructuring.

- Reach out to other businesses. If possible, try and reach out to other businesses that have previously worked with venture debt lenders. This way, you can get positive references as well as valuable insight into what you can expect from working with a particular venture debt lender.

Conclusion

And that’s about all you need to know about venture debt.

By now, you should have a better understanding of venture debt and whether raising venture debt is the right financing option for your startup.

On top of that, now you know exactly how to choose the right venture debt lender to fund your business!

Before you go, though, here’s a quick recap of the key points mentioned in this article:

- Venture debt is a financing option that’s available to startups and growth-stage companies, typically in the form of an up to 3-year term loan that comes with an interest rate and warrants for venture debt lenders.

- Venture debts are often cheaper, more flexible, quicker to obtain, and more accessible to startups than other financing options.

- To raise venture debt, you should first select a venture debt lender with the most favorable terms and conditions, which are usually outlined in the venture debt term sheet.

- Venture debt shouldn’t be used as a last resort if you see that your company won’t be able to pay off the debt.

- Whether you choose a bank or non-bank venture debt lender, make sure they’re reputable, dependable, and make an excellent business partner.

Recent Articles

How Sierra Achieved $200M in Revenue by Mastering Conversational Intelligence

In the dynamic world of SaaS, the journey of Sierra is nothing short of remarkable. The company, operating within the…

How 1Mind Achieved $6M Revenue in 18 Months Using AI Agents

Introduction: The Rise of 1Mind The rapidly evolving landscape of AI technology has witnessed the emergence of several transformative companies,…

How 1Mind Achieved Rapid Revenue Growth with AI-Powered Sales Solutions

In the ever-evolving world of technology, few companies have managed to disrupt traditional sales and marketing processes as effectively as…